Market Insights: Tech Beta Rising

Source: Zephyr.

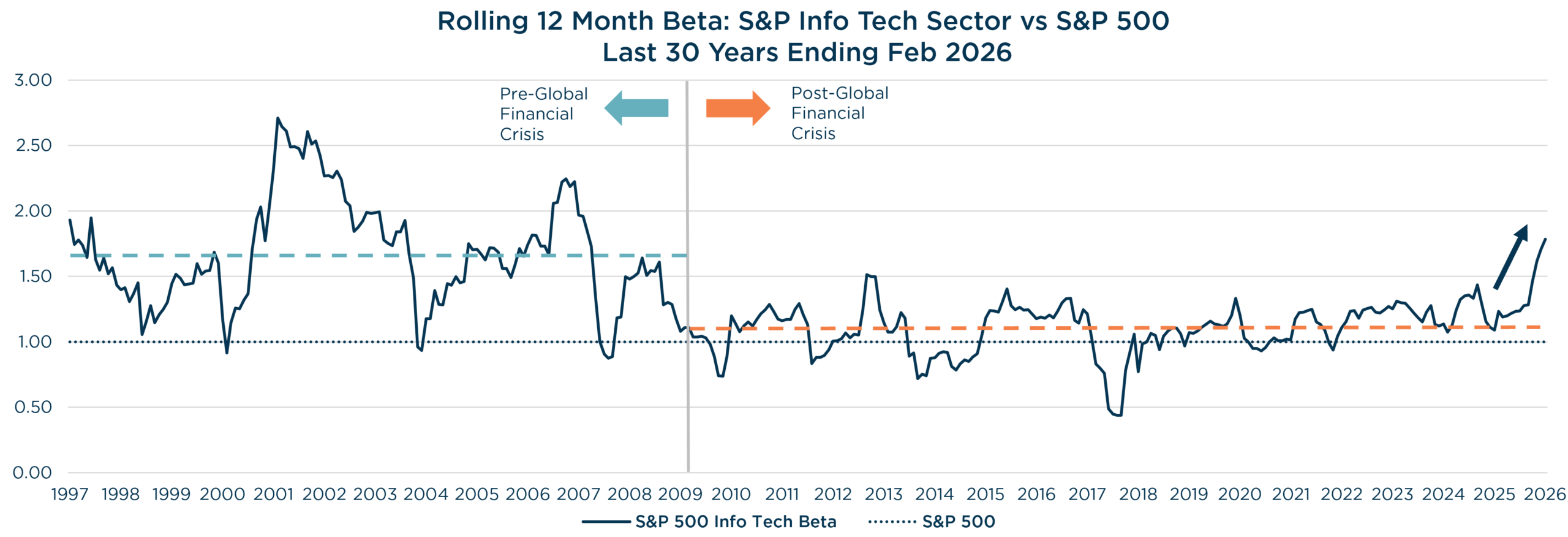

A Familiar Pattern Re-emerges

The Information Technology sector has historically been characterized by higher volatility than the broader market, a pattern that reflects the sector’s defining features: rapid innovation, constant disruption, and larger swings in valuations compared with other market segments. This relationship between technology and volatility is not a flaw but rather a natural consequence of investing in businesses operating at the frontier of innovation.

Over the past 30 years, the rolling 12-month beta for the Information Technology sector within the S&P 500 has averaged approximately 1.34. In statistical terms, this means that when the broader market moves, technology stocks have historically moved about 34% more. During market advances, this amplification works in investors’ favor. During declines, it works against them.

For much of the past 15 years, however, this historical pattern appeared to have changed. Technology stocks exhibited lower volatility than their long-term averages suggested, at times even providing defensive characteristics during market stress. This anomaly led many investors to reconsider technology’s role in portfolio construction, viewing the sector not just as a growth engine but as a stable core holding.

Recent market behavior suggests this period may have been the exception rather than the new rule. Since 2022, technology stocks have struggled during market pullbacks, and their volatility characteristics appear to be reverting toward historical norms.

The 2025 Speculative Surge

To understand the current state of down-cap indexes, it’s important to recognize what drove performance throughout 2025. The year was characterized by massive outperformance from higher-volatility and more speculative names. Two primary themes dominated: enthusiasm around artificial intelligence applications and a perceived thawing of opportunities within the biopharma space.

Companies positioned at the intersection of these narratives, whether through actual business operations or market perception, experienced significant multiple expansion. Investors, eager to capture exposure to transformative technologies and breakthrough therapies, bid up valuations for businesses that promised participation in these secular trends.

The result was a year in which speculation often trumped fundamentals. Companies with limited profitability, or in many cases ongoing losses, saw their valuations soar based on future potential rather than current earnings power. This dynamic fundamentally altered the composition of small and mid-cap benchmarks.

The Post-Crisis Anomaly

Several factors contributed to technology’s unusually muted volatility following the Global Financial Crisis. Extraordinarily low interest rates created a valuation environment that particularly benefited long-duration assets like growth stocks. When discount rates approach zero, the present value of distant future cash flows rises substantially, supporting elevated valuations even during periods of market stress.

The extended economic expansion that followed the financial crisis provided a supportive backdrop for technology business models. Cloud computing, software-as-a-service, digital advertising, and e-commerce all benefited from secular tailwinds that proved remarkably resilient. As technology stocks performed well, more capital flowed into the sector, providing price support even during broader market weakness.

This confluence of factors created an environment where technology stocks often outperformed during market downturns, defying their historical volatility characteristics. The 2015 Flash Crash and the 2020 Covid selloff both saw technology stocks hold up relatively well or recover quickly.

A Return to Historical Patterns

The environment that supported technology’s anomalous defensive characteristics has changed materially. Interest rates have risen from historic lows, ending the zero-rate regime that particularly benefited long-duration growth assets. These macro shifts have coincided with a change in how technology stocks behave during market stress.

Since 2022, market pullbacks have seen technology underperform rather than provide defensive ballast. The sector’s beta, which had compressed during the post-crisis period, appears to be reverting toward its long-term average. This reversion should not be surprising. Technology remains a sector characterized by rapid change, intense competition, and significant uncertainty. Valuations, which expanded significantly during the low-rate environment, now face greater scrutiny.

Recent market behavior suggests that investors are once again treating technology stocks with the volatility consideration they historically warranted. When market sentiment turns cautious, capital may flow away from higher-beta sectors more quickly.

The Concentration Complication

This return to more typical volatility patterns occurs at a particularly notable moment. Technology’s weight within major indexes like the S&P 500 remains at historically elevated levels. The sector that now exhibits higher beta characteristics also represents the largest concentration within the benchmarks that underpin much of the passive investing industry.

For investors who have gained technology exposure through index funds or ETFs, this combination creates a challenging dynamic. Not only are they significantly concentrated in a single sector, but that sector now appears to be returning to its historical volatility profile. What was once positioned as broad market exposure increasingly resembles a concentrated bet on technology with heightened volatility.

This reality extends beyond purely passive investors. Many active managers maintain relatively low active share versus their benchmarks, meaning they too carry substantial technology exposure that closely mirrors index weights. During periods when technology underperforms, portfolios heavily weighted to the sector will likely experience amplified drawdowns relative to a more balanced approach.

Managing Concentration and Volatility

Given these dynamics, investors may want to evaluate whether their portfolio construction appropriately accounts for both technology’s concentration within major indexes and the sector’s return to more typical volatility patterns.

Understanding actual sector exposure matters more than understanding strategy labels. An investor who holds multiple large-cap managers may believe they have achieved diversification, when in reality each manager closely tracks an index where technology represents the dominant weight. The effective technology exposure across the portfolio may be far higher than intended.

The quality of technology holdings also deserves consideration. Not all technology exposure is equivalent. Companies with strong competitive positions, proven business models, and reasonable valuations present different risk profiles than speculative businesses trading on narrative appeal. In a higher-volatility environment, these quality distinctions become more important.

Genuine diversification requires holding companies and sectors that behave differently from one another. When a single sector dominates index weights and exhibits elevated volatility, the benefits of diversification diminish. Portfolios constructed with meaningful differentiation from technology-heavy benchmarks may provide more resilient characteristics across various market environments.

An Active Approach to U.S. Large-Cap Investing

At The London Company, we believe the current environment strengthens the case for active management in U.S. large-cap equities. Our investment approach emphasizes business quality across all sectors, valuation discipline, and high active share that deliberately differentiates from technology-heavy benchmarks.

We focus on identifying companies with sustainable competitive advantages, strong balance sheets, and reasonable valuations. This approach inherently limits exposure to the most expensive segments of the market and creates portfolios that look and behave differently from concentrated indexes. While we may own quality technology businesses, our portfolio weight in the sector typically differs materially from benchmark weights.

In an environment where the largest sector concentration exhibits heightened volatility, we believe this differentiated approach can provide what passive strategies increasingly struggle to deliver: genuine diversification, quality orientation, and valuation discipline. Historical patterns have tended to reassert themselves over time, and building portfolios that account for this reality seems prudent given current concentration levels within major indexes.

Read More Thought Capital

from The London Company