Insights from the CIO

Founder, Chairman, and Chief Investment Officer

Investment Takeaways

-

According to Warren Buffett, markets are “a church with a casino attached,” and recently he has “never seen people in a more gambling mood.” The current backdrop has plenty of examples that support that observation.

-

Many of the classical hallmarks of conservative investing (dividends, defensive sectors, & lower volatility market factors) sit at multi-decade lows in popularity, while speculative flows reach record highs.

-

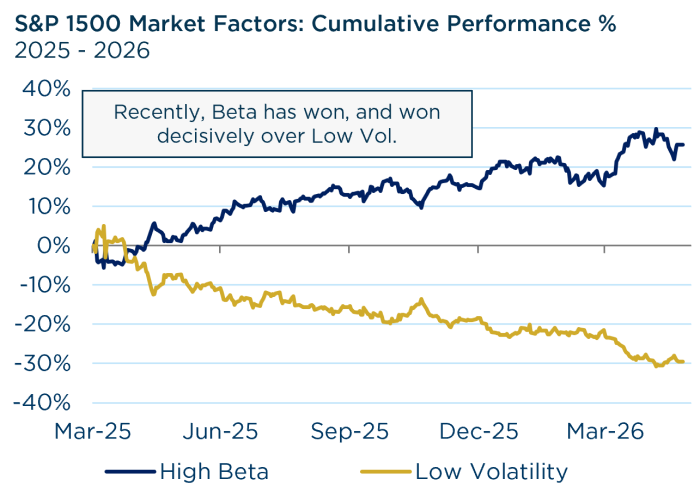

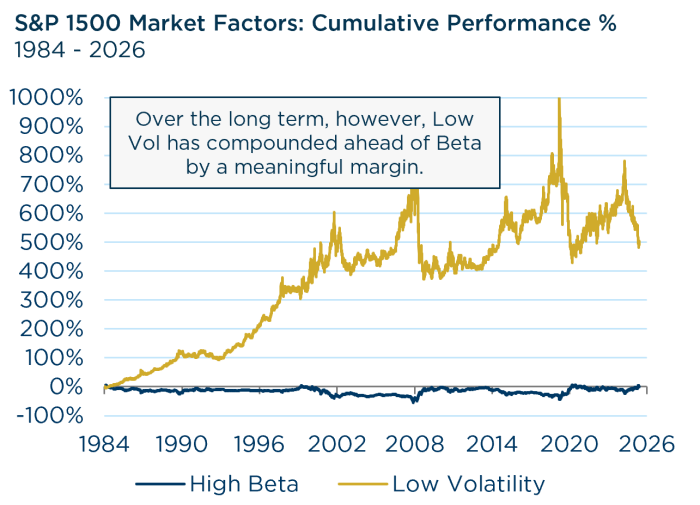

Risk factors, like High Beta, have decisively beaten Low Volatility recently. Over the long term, however, Low Volatility factors have compounded ahead of Beta by a meaningful margin.

-

Our outlook is broadly constructive, but the headwinds facing today’s leadership are accumulating in ways we believe matter. Our portfolios prioritize quality, balance sheet strength, and reasonable valuation, and they are trading at some of their most attractive levels in years.

Perspectives on the Market

Warren Buffett has used the same line for years to describe the stock market: a church with a casino attached. The church is for patient owners of businesses. The casino is for everyone else. What caught our attention was his recent addendum. He noted that he has “never seen people in a more gambling mood.” When the man who has watched markets for eight decades says the casino has gotten loud, it is worth pausing to look around.

From our vantage point, the pews are empty, and the tables are full.

The Pews are Empty

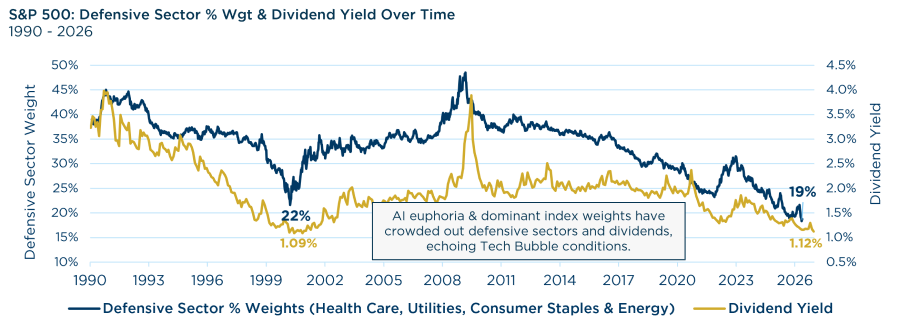

By any reasonable measure, the classical signposts of conservative equity investing are deeply out of favor. The S&P 500 dividend yield has fallen to roughly 1.1%, a whisker above the all-time low set in March 2000, and the combined weight of the traditional defensive sectors (health care, consumer staples, utilities, and energy) sits near 19%—an all-time low.

The phenomenon extends well beyond dividends and defensive sectors. Low-volatility equities trade at meaningful relative discounts to the broader market, and many high-quality companies with durable competitive advantages and strong balance sheets have watched their multiples compress while speculative names re-rated higher on little more than narrative. Across the attributes that have historically defined prudent equity investing—quality, financial flexibility, stability, reasonable valuation, and yield—the message from the market has been the same: not interested.

We view this as an opportunity rather than a verdict. Our own portfolios, which prioritize precisely these characteristics, are trading at some of their most attractive valuations in years. Markets have a long-running habit of pricing things based on how they have performed most recently, and right now they are pricing prudence as if it has limited value & no excitement.

Source: Strategas & Piper Sandler. Sector data from 2/2/90 – 5/22/26 and yield data from 12/31/89 – 5/29/26. Past performance should not be taken as a guarantee of future performance.

Source: Strategas & Piper Sandler. Sector data from 2/2/90 – 5/22/26 and yield data from 12/31/89 – 5/29/26. Past performance should not be taken as a guarantee of future performance.

A Tour of the Casino Floor

If the pews tell one story, the tables tell another. Recently, an active ETF was launched to capitalize on surging AI-driven demand for global memory & chip storage. That ETF, the Roundhill Memory ETF (ticker: DRAM), launched on April 1. With just 9 holdings, DRAM has amassed over $13 billion in two months, one of the fastest ramps for any investment product on record. Memory chips, it bears noting, have historically traded like a commodity, with the cyclicality to match. Other examples of speculative fervor include daily Options volume, which sits at all-time highs, much of it concentrated in zero-day contracts that expire the same session they are bought. Leveraged ETF assets continue to swell. Additionally, the expected combined IPO value of SpaceX, OpenAI, and Anthropic alone may approach $4 trillion, which, adjusted for inflation, exceeds the value of every Dot-Com IPO between 1995 and 2000 combined. When prices, flows, and behavior detach this far from underlying economics, history suggests they tend to reattach, and they rarely do so gently.

The Short Cycle and the Long Arc

The cumulative one-year performance of High Beta versus Low Volatility looks roughly like what you would expect from the conditions described above. Zoom out, however, and the relationship is notably flipped (see charts below). The path was unglamorous, but the destination was not.

This is the part of the story that gets lost in any given quarter. Low Volatility is, almost by definition, a strategy that underperforms in exciting markets and outperforms across full cycles, and that is the contract rather than the flaw. Investors who own these characteristics are not betting against innovation. They are accepting a smoother ride in exchange for missing some of the spikes, with the expectation that they will also miss some of the drops. Over the long term, that contract has paid.

Source: Piper Sandler. Data from 3/31/25 – 5/29/26. Measures the forward price return of the companies in the S&P 1500 high & low quintile baskets of stocks by factor. Factors are sector neutral. Quintile baskets are rebalanced monthly at the beginning of each month. Past performance should not be taken as a guarantee of future performance.

Source: Piper Sandler. Data from 12/31/84 – 5/29/26. Measures the forward price return of the companies in the S&P 1500 high & low quintile baskets of stocks by factor. Factors are sector neutral. Quintile baskets are rebalanced monthly at the beginning of each month. Past performance should not be taken as a guarantee of future performance.

Source: Piper Sandler. Data from 12/31/84 – 5/29/26. Measures the forward price return of the companies in the S&P 1500 high & low quintile baskets of stocks by factor. Factors are sector neutral. Quintile baskets are rebalanced monthly at the beginning of each month. Past performance should not be taken as a guarantee of future performance.

Our Posture

Our outlook is broadly constructive, with a healthy earnings backdrop, resilient economic data, and meaningful long-term productivity gains likely from artificial intelligence. That said, the headwinds facing today’s leadership are accumulating in ways we believe matter. The AI capex boom is real but fragile, free cash flow at the hyperscalers has turned negative even as their stocks compound. Geopolitics & tariff clarity are anything but stable, and energy prices remain elevated. Further rate cuts may prove challenging against a backdrop of stubbornly elevated inflation, low unemployment, and resilient economic activity. Layer on historic index concentration and valuations that require near-flawless execution, and the cumulative case for discipline becomes hard to ignore.

In Summary

Every market has both wings of Buffett’s building, and the casino and the church have always coexisted. What changes is the foot traffic. Right now, the slot machines are loud enough that you can hear them from the back pew, and the collection plate has gone light. We are not predicting when the music slows because no one can. What we can do is what we have always done: own quality businesses, pay reasonable prices, and let compounding do its quiet work. We know which side of the building we want to be in when the bill comes due.

View Our Strategies

See the latest performance data